Higher Education, higher costs?

Young graduates are living in a very high tax country. We need to look to reforms rather than simply add to their burden

One of my favourite films is Educating Rita. It’s a wonderful, bittersweet movie, but the premise of the film probably won’t make any sense to young people now.

For younger readers, the main premise is: a young working-class woman goes to university!

That’s it. That’s the premise.

When written in 1980, that worked, because it would have been an unusual thing.

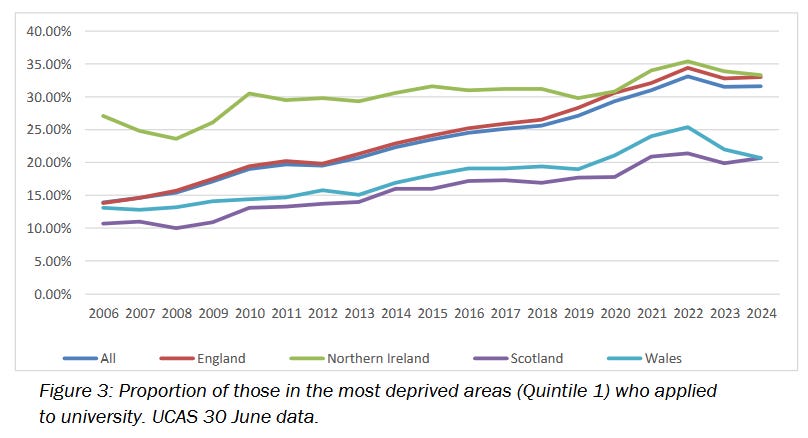

It isn’t now. The number of people going to university has exploded - fastest in England, which has gone furthest on fees. From 3.4% in 1950, it rose to 8.4% in 1970, and 19.3% in 1990. By 2020 53% of young people went to university.

In England there has been particularly strong growth in the number of university applicants from the poorest fifth of areas, with the proportion more than doubling.1

Much of the growth of HE is a very good thing. My siblings and I were the first generation to go to university in our family.

Most people who go love it. I know I did. And the benefits of Higher Education go beyond the teaching and research in the university. Not just the businesses who partner up with universities, but the wider benefits to the local community in ways great and small. In my teenage years I could walk into the library in Huddersfield University (nonchalantly trying to look like a student) and read all kinds of wonderful things. It’s a happy memory.

So why are we not supporting further tuition fee increases?

Many things have moved on since the launch of fees under the coalition, and this piece looks at some of them.

Put simply, young graduates are living in a very high tax country. We now need to look to reforms rather than simply add to their burden.

Tuition fees: why worry now?

A university education is not cheap. The government just raised tuition fees to £9,535 a year. The maximum maintenance loan for people not living at home is £10,227 - or £13,348 in London2. So after a typical three-year degree you need to pay back up to £59,286 - or £68,649 in London. That’s a lot of money.

Given this government has already increased fees once, there must be a decent chance they will go up each year from now on.

If we assume they continue to rise with the OBR inflation forecast3 then by the end of this Parliament (2029/30), fees will be just under £10,700 a year, and maintenance loans up to over £11,400 (or £14,900 in London). So that’s a total to repay of about £66,400 after 3 years, or up to £76,900 in London.

As it happens, this year’s fees hike has not made universities better off - because the cost of the National Insurance hike almost wipes out the benefits to the sector of the decision to increase tuition fees.

Effectively one broken promise (on fees) is paying for another broken promise (on tax).

It isn’t just that this is the opposite of what Labour promised - see their pledge above.

It’s something deeper. Ever since David Willetts’ seminal book The Pinch we have been worrying that young people can’t get on in life. That they have worse prospects than their parents, aren’t able to get a house and so on.

And yet to pay for the expansion of HE, we have created a situation in which young graduates live in a very high tax country.

Repay your loans on the minimum wage

Though there is still taxpayer subsidy, since 1998 steadily more and more of the burden has been shouldered by graduates themselves. The OBR says the share of loans that count as public expenditure will be just over a third in future. 65% of those starting undergraduates are now expected to repay their loan in full - a big increase.

This is partly because the repayment period has been extended to 40 years after the point where you are supposed to start repaying, meaning that in future there will be over-60s still paying off student loans.

It’s also because the repayment threshold has come down. For new borrowers, thresholds were reduced to £25,000 in 2023-24, and then held constant. This means the threshold is falling in real terms.

Compare the repayment threshold to the minimum wage. In 2005 you would not have started repaying your loans unless you were earning 30% more than a full-time worker on the minimum wage. From April 2025 new grads (on plan 5) will be liable to repay if they earn 2% less than someone working full-time on the minimum wage4.

Growing numbers have postgraduate loans too. For them the loan repayment threshold has been £21,000 since 2019/20 - so they have been repaying even in a minimum wage job since 2023.

The graduate loans system is not quite a graduate tax yet, but it sure does feel a lot like one. It is still income-contingent in that if you don’t work at all you don’t pay.

But the numbers working-but-not-repaying will be very small in future, which is a big change compared to when they were launched.

The system also produces some incredibly high marginal tax rates for young people. If you also have a postgraduate loan, or if you get into the High Income Child Benefit Charge (HICBC) then you can face absolutely insane marginal tax rates on middling incomes.

Very sadly, the new government have abandoned plans to reform the HICBC, so this problem is now not going away any time soon.

Graduates are having 51% of their income taxed away at just £50,000 of earnings, a sum which won’t feel like being rich if you are renting in an expensive city.

And over £60,000 of earnings graduates (and particularly postgraduates) with kids are facing marginal rates in the 58-73% range - the sorts of rates that used to apply only to supertaxes on the very wealthy.

Is it worth it from an economic point of view?

Another way things have changed since the launch of fees is that we have much better data.

On average graduates earn more than non-graduates - no great surprise there. They generally did better at school too. But what is the value added of the degree compared to something else?

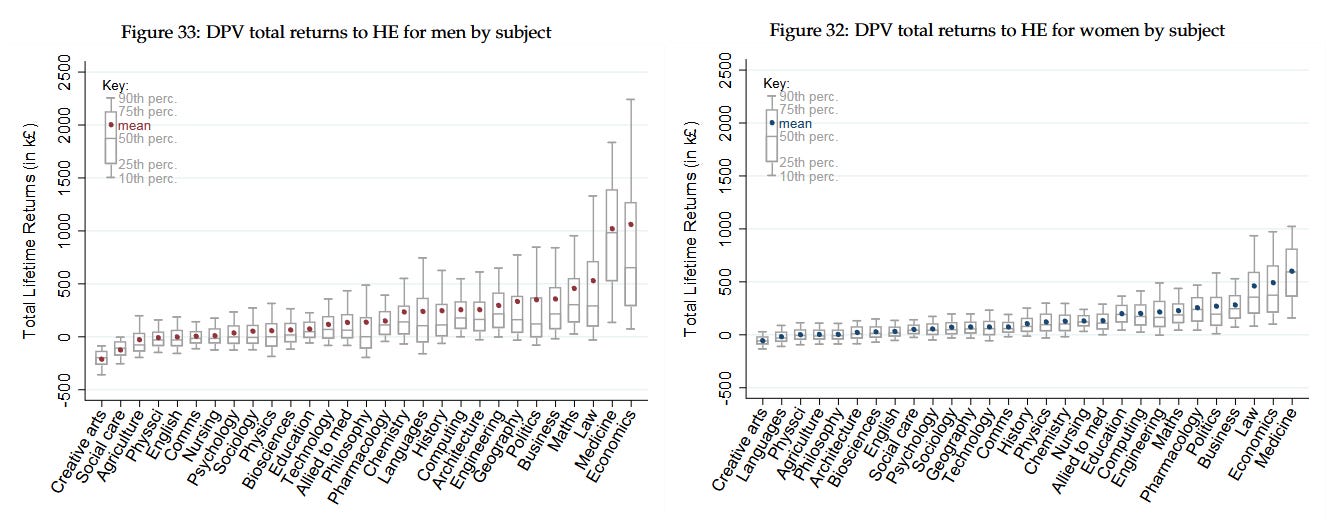

The Institute for Fiscal Studies have taken the deepest look at this, looking at how graduate earnings are evolving for different institutions and types of courses, and trying to compare that to a counterfactual of people with similar prior characteristics. They looked at how many people saw their earnings boosted and what the costs were. They then worked out what the net benefit was for the individual, the taxpayer, and also combined these perspectives to get a sort of final score.

Their conclusion in a 2020 report was that:

“seen over the whole lifetime, we estimate that total returns will be negative for around 30% of both men and women.”

And that

“While getting an undergraduate degree is worthwhile financially for most students, there is significant variation across subjects. Some subjects, such as medicine, law and economics, offer a springboard to very lucrative careers… However, a significant minority of mostly men are likely to not see positive returns as a result of going to university… lifetime earnings returns remain low or negative for subjects such as creative arts and English.”

Now, this data needs handling with care (see Annex below).

But these sorts of numbers deserve to grab our attention. As I’ve written before, the demographic outlook for the UK means the public finances will be subject to crushing, tectonic forces.

Whether you want to cut taxes and raise living standards, or spend more on public services, there is no magic pile of cash lying around waiting to make your dreams come true. So where there are significant opportunities to spend better, we have to look seriously at them.

Of course, there is a perfectly reasonable case for spending on Higher Education that doesn’t have a good economic return. It’s roughly the same as the case for spending on the arts. It doesn’t boost GDP, but does give people pleasure. This is a perfectly reasonable argument. But there are two comebacks.

First, we should avoid assuming that things that are more economically useful are not also beautiful, increasing, and intrinsically valuable. It’s interesting to know that the word “Lent” is a corruption of the Anglo Saxon for “lengthen” (because it falls in spring when plants are growing). But it is also cool to know what a Giffen good is, or how monoclonal antibodies work, or how to build an ion drive.

Second, as with the arts, there’s probably a limit on how much we want to spend on such consciously-noneconomic courses. With every other priority looking for resources (health, schools, crime… the cost of living) we can afford some of this: but how much do we want to spend on it?

Currently £20 billion per year is loaned to higher education students in England, which will increase to about 24.5 billion by 20285. If around 30% of that was not working out from an economic point of view… (£6bn+) that would be a lot of money - about 10 times what the Arts Council spends every year.

What the market did - and didn’t - do

At the start of fees it was hoped there would be price competition as part of a lively market. Some places would charge £3000, some £6,000 some £9,000… while exciting new innovative models and ways of doing things would proliferate…

This was a reasonable hope. Higher Education is probably the part of education that is potentially most promising for productivity improvements. Nursery care will always be people-intensive. There’s no other way to deliver a timely cuddle to a three-year-old who just tripped over. Small children cannot self-teach. But higher education should in theory be more open to new ways of doing things.

And yet… things didn’t pan out that way. Instead, fees immediately clustered at the maximum amount, and trad three-year courses still absolutely dominate.

Why? The HE market is all about brands - and unis have feared that any move to do things differently will undermine their brand.

The problem is that unlike a car or a loaf of bread, a university education is something most people only buy once, at age 17, and it is much more difficult to discern better from worse. Indeed, much of the value to the “consumer” is about how other people (like employers) see it anyway. It is interesting that the current “market” has not (yet) delivered innovative new ways of delivering HE at lower cost / higher quality. For me, this untapped potential for innovation is another reason to look first to reform, rather than our first resort being to simply increase the amounts young people must pay.

Some still argue that there is nothing to solve here: that a free market and “consumer choice” are sufficient to discipline the growth of lower-value HE. I think given the massive information asymmetries, relying on the choices of 16/17 year olds to create a perfect market seems unrealistic. Many will (unsurprisingly) choose on the basis of what they like at school, not by thinking about their earnings at age 50.

Would it really be an appalling constraint on their choice if, looking through university prospectuses for the first time, 16 year olds were faced with a slightly different array of choices eligible for government support? There are around 50,000 different university courses available at the moment. If we could find a way to ensure slightly more young people did things with better returns rather than worse, that would hardly be a tyrannical taking-away of choice. Indeed, they would have better choices: at present many end up in debt and feeling they have been mis-sold.

The HE market certainly has responded to incentives in some ways. The most obvious has been the explosive growth in first and 2:1 awards. Measures taken by ministers in the last couple of years seem to have finally paused the inflation, but lecturers still report pressure to raise student satisfaction by handing out higher grades.

The challenge is to set up the incentives in ways that drive the behaviours we want, not the ones we don’t.

A tangled web: the end of number controls

Another huge way that the picture has changed since the launch of fees is the end of number controls. Announced in 2013 and effective from 2015, the end of the longstanding controls on student numbers on different courses has had positive effects, but also negative ones.

As the balance of resources has shifted from public spending and teaching grants over to tuition fees - and particularly since number controls were abolished in 2015 - Ministers have found they have less and less leverage over what taxpayers’ money ends up being spent on.

If a course is cheap to provide relative to fees there is a strong incentive to grow it. There is no connection between the private benefit to a university of putting on a course and the net cost to the taxpayer. Profits are privatised, but losses socialised.

As a result an opaque and tangled web of cross-subsidies has emerged - what matters is whether a course is good value for the institution providing it, rather than whether it is good value for students and taxpayers.

Conclusion

I’m very sympathetic to the plight of staff at universities where the leadership have got them into financial difficulties: be it through taking out ill-judged expensive loans or spending on fancy buildings, or overdependence on one group of overseas students.

And I’m sympathetic to universities and lecturers more generally. It’s a hugely important job and it’s not the case that unis are all awash with cash: though it is worth saying that upfront real-terms funding per student is still substantially above the level of the pre-fees era, even as numbers have exploded.

There are many wonderful, valuable courses in HE I hope will expand and prosper.

But young people in Britain have it tough, and the large repayments and high marginal rates they face are an important part of that.

We need to do right by our universities, but also by young people. I believe through reforms there’s scope to get them a better deal. We should look to reforms first, rather than simply increase the burden on young people.

Annex: reading the LEO data

There are many things to say about the Longitudinal Education Outcomes (LEO) data, which needs care in interpretation.

There’s a regional question: if more of the graduates of a university in a poorer region stay local they will likely have lower earnings – even if their real standard of living isn’t much different because of lower housing costs. But their earnings are being compared to a national benchmark, which might be unfair.

There is uncertainty too. The system is only so old – we can only observe graduates so far after graduation. When the IFS update this work we will have more, but there’s some (well informed) estimation going on.

As with all kinds of other investments, the choice of discount rate matters a lot too, and there are no knock-down arguments about what rate is the right one to use. The IFS numbers I have replicated here use the Treasury Green Book Rate, but you could argue for another.

There are also arguments about the impact of childbearing and the meaning of the large difference in graduate premiums for men and women. A much larger share of men have negative lifetime returns (while a minority do spectacularly).

Multiple studies find that people with higher education have fewer children and have them later. There have been studies that look at the interaction of childbearing and earnings - controlling for this would potentially make the numbers for women look more like those for men, and the graduate premium lower.

There are also uncertainties about future earnings growth. The higher it is the more likely it is to offset the upfront costs - and vice versa.

No measure is perfect - but the LEO data gives us probably the best we have. There are uncertainties in both directions, but I don’t regard these limitations as an excuse to do nothing: this is better and more meaningful data than we have in many other fields of policy: we should just use it with care.

The same trends are visible on other metrics. The relative growth among FSM pupils is much greater than among non-FSM. On the POLAR metric of low participation neighbourhoods, the participation gap between the top and bottom fifth has shrunk in absolute and relative terms.

The maintenance loan is dependent on family income - not everyone is entitled the maximum amount.

Using RPIX as the measure of inflation.

Plan 5 loans started in 2023 so they will mainly start working in two years time.

It’s once again incredible to see you write a piece as though you are a mere dispassionate observer, rather than someone who supported 14 years of a government that did nothing but make these problems worse and worse.

I mean, you could just say “sorry for my part in this shitshow”, couldn’t you?

Thanks for a highly informative piece. The framing of human education as a purely transactional material good is simply wrong. Within this limited neo liberal ideology the final destination must be the end of all cultural creation to be replaced by numbers based automata. The end of humanitarian education and the embracing of a society built around abstract transactionalism. We are already too far down this dystopian rabbit hole with a Single Tranferable Political Party of Gradgrinds restructuring society. It is no wonder so many are choosing to take their kids out of school. As true intelligence is increasingly being pathologised as neurodivergent by systemic homogeneity.