What will Rachel Reeves do in the budget?

Will she keep her pre-election promises?

This post is going to look at four issues in the forthcoming Budget:

Borrowing;

Tax;

The politics of the in-year pressures;

The big picture argument about economic policy.

Let’s jump right in.

(A) Borrowing

Before the election the Chancellor implied she would stick with the current debt and deficit definitions. As Bloomberg reported:

Last November, Reeves told reporters she was “not going to fiddle the figures or make something to get different results” when asked whether she would consider using the easier debt target. “We will use the same models the government uses,” she said.

But in recent weeks there have been numerous briefings that the Government will change the definition exactly in order to get different results and borrow more. The Guardian reported that:

“One option for Reeves is to change the debt measurement to account for the value of the assets the government holds, such as roads, schools and hospitals. Measuring the net worth or the net financial liabilities held by the government could give the chancellor room to borrow as much as £50bn more than currently planned, although some officials worry it would spark a bond market sell-off, with the Treasury left to pick up the bill.

Reeves has talked privately about taking the less radical option of keeping the debt rule in place but excluding losses from the Bank of England from the debt calculation, as well as any extra borrowing used to set up public institutions such as the national wealth fund. This would free up a more modest amount of between £10bn and £20bn.”

The latter of these is being spun by government as the “moderate” option. But it still opens up a lot more borrowing, and potentially a lot more than the figures quoted above by the Guardian.

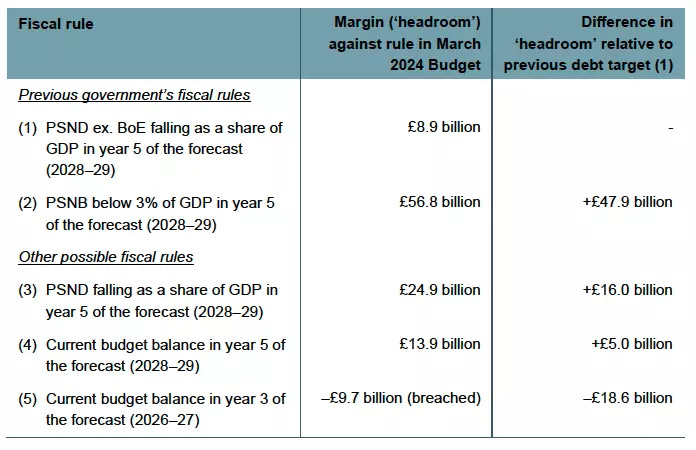

The last government had a goal for both debt and deficit. To get Public Sector Net Debt (excluding the Bank of England) falling and get Public Sector Net Borrowing below 3% GDP by year five of the forecast.

Labour’s manifesto said that:

the current budget (i.e. excluding capital spending) must “move into balance”

debt must be falling as a share of the economy by the fifth year of the forecast.

The IFS have an explainer on different measures of borrowing here.

The IFS produce some figures for how much extra headroom there would have been on the basis of the previous government’s plans, if it had used a different definition of debt including the Bank of England. They note that there would have been £16 billion more headroom in the final year on those plans.

But, as the IFS also note, these numbers are all on the last government’s plans. In reality this “debt-falling-in-the-final-year” target leaves Labour a lot more latitude than just £16 billion. In fact, they note that this debt rule is unlikely to bite much at all:

“If the government does tweak its debt target, the commitment to achieving current budget balance could take on greater significance and become the primary binding constraint on tax and spending decisions.”

This seems right to me. The £16 billion above is just the difference between the two slopes in the grey area below. As long as in the final year debt is falling then the level of debt can be quite a lot higher than it is now, and she can still say her rule is met.

The forecast will roll forward another year in the budget which may will help too.

The government claims it will “only borrow to invest”.

But the target of a current budget balance in five years time which is supposed to enforce this principle is very weak.

You can frontload current (day to day) spending and backload revenue raisers and overall borrow a lot more in the meantime - as long as on paper your future tax raising plans and future spending match up in the final year of the forecast.

And if you go off track at some point in the years ahead you can just come up with new plans on paper. The point where balance has to be achieved is always five years away. It’s like St Augustine, wishing to be virtuous, “but not yet.”

For what it’s worth, in March the current budget was in surplus in the final year (28/29) with £14 billion of headroom - and rolling forward another year there may be more. This already creates space for more borrowing for day to day spending, as well as more capital spending. That space gets bigger if you can pencil in some revenue raisers for 2030 and beyond. Under this target you can always revise those tax increases and kick the can down the road if they start to seem impossible.

So there is a lot of scope within the government’s rules to borrow more.

As the IFS note:

“If the government wants to borrow more and spend more, it would ideally make the case for doing so on its own terms, rather than hide behind fiscal jiggery-pokery.”

On Budget day HMT will hope to dazzle journos with complex arguments about APF repayments, crystalised losses and other “Treasury Magic”.

But at the end of the day, this is just borrowing more.

Journalists will just look through it to see: what is Public Sector Net Debt at the end of the forecast? What is borrowing as a share of GDP each year? Does overall debt still fall as a share of GDP after this year? I will come back to whether more debt-funded borrowing is a good idea later, but first, tax.

(B) Tax

While I think Reeves may do more by just borrowing than people are expecting, she seems likely to raise tax too. The overall tax burden is already at the highest level since 1950, so further increases will take us into uncharted territory.

Page 21 of the Labour manifesto said they would not raise taxes ON working people (my emphasis). It says:

“Labour will not increase taxes on working people, which is why we will not increase National Insurance, the basic, higher, or additional rates of Income Tax, or VAT.”

But a number of the tax increases Reeves is looking definitely are taxes on working people.

If she jacks them up then, as with the promise not to redefine borrowing or fiddle the figures, many people will feel this promise has been broken.

Dan Neidle has a useful long list of measures Reeves might want to pursue. There are so many possibilities I won’t get into lots of them.

But a common political problem is that many taxes fall “on working people”. For example, in answer to a written question I tabled, HMT say 50% of those liable to Capital Gains Tax are working. So will they be excluded from any increase in CGT?

Reeves’ search for new tax measures is made even more urgent because a lot of the tax measures which Labour proposed in opposition have wilted under scrutiny by HMT and the OBR in recent weeks. The numbers didn’t add up to their spending ambitions in the first place, but there’s been a litany of stories about plans being dropped or revised back:

“Rachel Reeves is rethinking parts of Labour’s crackdown on non-dom tax status over concerns that the plans will not raise any money.” (Guardian, 27 September)

“Rachel Reeves, the UK chancellor, is not expected to hit private equity bosses with the top 45p tax rate in this month’s Budget… One government insider noted that Labour’s manifesto only committed Reeves to closing tax loopholes, not to a full 45 per cent tax rate. Another said: “There will be a compromise on this.” (FT, 6 October)

“Reeves had been considering reducing the 40% rate of tax relief that higher earners enjoy on pension contributions, in a move that could have raised £10bn a year. Public sector unions warned, however, that doing so would hit almost 1 million of their members.” (Guardian, 7 October)

“The UK’s biggest and richest private schools are in line for substantial financial windfalls as a consequence of the government’s plan to impose VAT on their fees, according to official new guidance issued by tax authorities.” (Observer, 12 October)

Whitehall sources say there is growing concern about the limited options for tax rises…“Some very big tax decisions are being left until very late in the day,” one senior source claimed. Another said the Treasury’s tax-raising plans were in “complete disarray”. (Guardian, 10 October)

What can she replace these opposition-era ideas with? In recent days Labour politicians have argued that increasing Employer National Insurance contributions would (a) not be a tax on working people and (b) not be a breach of their manifesto commitment.

Few are persuaded of either of these claims. Paul Johnson from the IFS says:

“It seems to me that would be a straightforward breach of a manifesto commitment. I went back and read the manifesto and it says very clearly ‘We will not raise rates of national insurance.’ It doesn’t specify employee national insurance.”

If Labour do increase National Insurance that will be a particular irony - it is in fact the one major tax which is exclusively “on working people” - pensioners pay income tax and VAT but not NICs.

Without wishing to be pedantic, it does matter that the manifesto says “on” working people. There is no doubt that ultimately employer NICs fall on working people.

As Helen Miller from the IFS has pointed out, Employer NICS:

“are a tax on the earnings of working people. In the long run, expect the majority of a rise in employer NICs to be passed on to workers in the form of lower wages.”

And the OBR already made this point. In their 2021 EFO (page 28) they noted that:

“While the statutory incidence of employer NICs… is on businesses, we assume the economic incidence of the tax is passed through entirely to lower real wages in the medium term”

On the same basis that Labour are saying NI isn’t a tax on working people you could also make the same argument about VAT. Technically it is businesses that pay VAT. But of course, everyone knows the ultimate impact is on us as individuals.

Labour hammered Philip Hammond for exactly this kind of definitional wriggling in 2017, when he tried to argue that the manifesto pledge not to increase NICs didn’t include the self-employed.

As Yvette Cooper thundered:

“Quite, quite incredible!! Did they not actually read their own manifesto....?”

After the pandemic the last government introduced the Health and Care Levy with a national insurance element to repair the battered public finances. Rachel Reeves was quick to slate this as a “jobs tax.” In October 2021 she said it was:

“so worrying that, at this crucial time, the Prime Minister and the Chancellor concocted a new jobs tax to arrive in the spring.”

She also said it was a broken promise. In March 2022 she said :

“Let us not forget that last March, a year into the pandemic, the Chancellor said, “We’re not going to raise the rates of income tax, national insurance, or VAT.” This is not just the wrong thing to do; it is a broken promise. It is a clear and flagrant breach of the Conservative party’s own manifesto.”

Given all this, I really wonder (despite all the briefing) whether they will really increase National Insurance. It seems so obviously a breach of their manifesto commitment that I just wonder if this isn’t a classic example of us all being played by HMT pre-budget misdirection.

But other tx options don’t look that great either.

Despite Reeves’ central narrative being about “increasing investment”, two of the other tax measures being tipped at the moment are taxes… on investment. Namely, Capital Gains Tax and pensions savings.

Various papers have reported on good authority that Reeves will use her budget to increase capital gains tax on the sale of shares and other assets but will not change the rate for second homes. The UK already has a problem about financing productive investments and has done a lot through regulation to push more savings into low-growth options like gilts. So this seems like an odd way to go if you want more investment in growth.

CGT is a spectacularly complex tax and there are many other options to raise money within it. Its complexity and opacity make me think it is one of the more likely places Labour will look for money. There are lots of variables to tweak and elements like the capital gains rebasing on death which they could abolish. I guess dead people are by definition not “working people”, though that rule’s there to avoid a dual hit of both IHT and CGT which might create some hard cases.

There’s also speculation that Reeves will (like Gordon Brown in his first Budget) move to tax pension savings more too. People have talked about the tax-free lump sum being reduced, or employer NICs being levied specifically on pension contributions. But if anything we need to save more for our pensions.

Lots of other familiar measures are floating about. You can look to reform Business and Agricultural Property Reliefs. But unless you have really big carve outs (which make the tax take much smaller) this would mean the end of the idea of the “family business” and the “family farm”, and would cause a big blowback.

(C) The politics of in-year pressures - the “22 billion”

Before the election Reeves said that she wouldn’t be able to feign surprise about the public finances:

Reeves admitted that — unlike previous incoming chancellors — she would be unable to arrive at the Treasury and claim she had looked inside the books and realised things were even worse than they looked from the outside, giving a flimsy excuse for immediate tax rises or spending cuts. “We’ve got the OBR now,” she noted, referring to the fiscal watchdog’s detailed and public scrutiny of the public finances. “We know things are in a pretty bad state,” she said. “You don’t need to win an election to find that out.”

Since the election they have done exactly that, repeatedly pushing the idea of a “£22 billion black hole.”

The Treasury are refusing to say how it arrives at this number, refusing a Freedom of Information request by the Financial Times.

The FT note that

The largest chunk of unaccounted spending is £8.6bn earmarked for “normal reserve claims”. The Treasury has said the £8.6bn includes items such as election funding, reclassification of the flood defences programme, and resettlement arrangements from Afghanistan — but has failed to quantify them. Tom Pope at the Institute for Government think-tank said it was “not unreasonable” to expect the Treasury to give details of the reserve claims.

We do know the biggest element of the “22 billion” (the doc is here) is £9.4bn of public sector pay awards. Now, you can say that some settlement was needed, and that it was going to be higher than average, but this is still a choice this government made (not the last one). The NICs cuts which Labour went along with were always obviously going to be contingent on tight public sector pay discipline.

There are real in-year pressures in there: £1.7 billion is military and civilian support for Ukraine. The biggie is £6.4bn of pressures in asylum and illegal migration.

I thought of that one the other day when it emerged that Labour are signing contracts to manage small boat arrivals for the next decade and are trying to find thousands of extra hotel beds for asylum seekers.

Now, I bow to no-one in my criticism of the last government’s policies on illegal immigration. But Labour’s position is nonsense too. They imply that if we just process people faster there will be no costs: all these people will no longer be a net cost to taxpayers.

That is very unlikely: those who arrive via this route are likely to have a large net cost even once granted asylum. A study at the University of Amsterdam calculated that, over a lifetime, the average asylum migrant costs the Dutch public more than £400,000. The UK government won’t even make such calculations.

Simply waving people through even faster makes the costs “disappear” into the wider welfare state and the government then refuses to publish data on welfare claims by nationality. But if waving more people increases the pull factors then it is likely to increase, not reduce, the real-world costs.

So there are some real presures in there but there are always in-year pressures. As Simon French has pointed out there is always variance against forecast spending - he notes there has been an average variation of £7.1bn over last six years, even excluding 2020. The most recent OBR Forecast Evaluation Report notes that on average its overall borrowing forecast for one year ahead is normally out by £12 billion (or 38.8 billion if you include the Covid years).

Where I really part ways with reeves is that the government has used the issue of in-year pressures to argue that it has inherited a terrible economic situation… which it couldn’t have possibly seen coming… which will therefore force it to do a bunch of things which it, er… definitely wasn’t planning to do all along.

During the Winter Fuel Payment row no-one has believed this line and I don’t think anyone will now. Paul Johnson has a good piece on the in-year pressures, (biffing both sides) in which he notes that:

“The chancellor cannot honestly announce a series of tax rises in her October budget, blame them on this hole that she has just discovered, and claim that she couldn’t have known pre-election that tax rises would be needed to maintain public services. That fact was obvious to all who cared to look.”

Even if we took Reeves’ claims totally at face value, still in the grand scheme of things Labour’s inheritance on the fiscal side is nothing compared to the levels of borrowing after the financial crisis, never mind Covid. Here’s her 22 bn (about 0.8% GDP) in the context of historic borrowing:

Here it is in the context of debt, which is a bit over 2.7 trillion this year.

To put it mildly, if she’s borrowing more, Reeves is going to have to have a hard job explaining why the in-year pressures this year represent economic apocalypse, but her own plans to greatly increase borrowing are totally fine and sensible.

Still, I would expect to see some more theatre around the in-year pressures at Budget.

In an attempt to dramatise the in-year pressures I can easily imagine Reeves announcing more powers for the OBR to monitor DEL forecasts in order to “make sure this never happens again”. The OBR are to produce a special report this Budget on the DEL forecast in the last Budget, so some kind of change in the process seems nailed on.

That’s all well and good, but I don’t think journos will be put off by this kind of distracting chaff if she if simultaneously borrowing a lot more. Which takes me on to…

(D) The big picture

I have written before about the crushing fiscal pressures that an ageing society is going to put the public finances under. Every year the OBR Fiscal Risks Report shows how, unless we change something, demographics will push down tax receipts, push up spending and set us on course for unsustainable, runaway debt levels:

I am all in favour of more investment in sensible things and in favour of increasing growth.

But given the considerations I worry about lots more government “investment” funded by more debt. There is a strong risk the “investments” won’t be growth-enhancing compared to leaving the money in the private sector.

Policies like auto-enrollment which have increased savings (and cut consumption) have been a great success.

Around the world successful governments have chosen to increase investment by restraining consumption. In Singapore the Central Provident Fund mandates savings with employer contributions of 17% pay and employee contributions of 20% (it used to be even higher!) Across Asian tiger economies savings and investment rates have been much higher than in the developed economies, a factor in their catchup growth. China has been the most extreme with saving (and investment) rates of 40-50% GDP compared to about 15% in the UK.

This is pretty hardcore, but is not radically different in principle to postwar Britain, where we deliberately reduced consumption (including through rationing) in order to create space for investment.

I wouldn’t advocate for anything so drastic. But I would advocate against the opposite.

As noted above there is speculation that Reeves will fund some of her increases in government spending by increasing taxes which hit saving and private investment. Instead of Asian-style save-to-invest, the long term effect of this would be cutting-investment-to-spend.

It has been interesting to watch the same group of people who were arguing for a borrow-to-invest splurge in the early 2010s to fix a supposed demand deficiency now argue for… exactly the same policy when the economy is at full capacity.

The UK does have an investment issue - but it’s in the business sector not government. Government investment as a share of GDP used to be lower than the US or Eurozone, but has caught up.

For that reason something like the Super-deduction (a tax break on business investment introduced under Jeremy Hunt) feels more on target than the sort of things the government is likely to “invest” the money in. Before it came in I had written for years about how the UK had thje least investment-friendly tax regime in the G20. The Super-deduction was a big step in the right direction, but there is more we can do.

In contrast a big priority the government is capital spending to support Ed Miliband’s agenda to dash to get to a Net Zero grid by 2030, which is likely to be very negative for growth.

For example, the government has already committed £22 billion into CCUS and hydrogen projects. I suspect that money would be more growth-enhancing if you just left it with companies to invest themselves rather than giving it to Ed Miliband.

Not every item of government capital spending is a good investment. Some parts of government current spending are good investments. And many of the best investments are more likely to happen if we change tax policy to help private investment, rather than have the government tax and spend more.

There is a sort of second-best argument whih says that politicians in Britain and the developed world are too weedy to make the savings elsewhere to increase investment so we should just borrow more anyway.

But the truth is that without a hard budget constraint, reforms in government don’t happen.

For example: where is the government’s plan on welfare? Working age welfare needs massive reform:

…but that won’t happen if there is an easy way out through more borrowing.

Another example: where is the government’s plan on public sector productivity? Public Sector productivity fell from 1997 to 2010 and only grew during the period of relative fiscal restraint 2010-19. It is still recovering from the pandemic.

No budget constraint, no hard choices, no progress. To pick just one example: there were 384,000 civil servants in 2016, and 513,000 in 2024. Is government so much better for this increase?

Conclusion

Labour’s fiscal rules allow them a lot of scope to borrow more and still say they are hitting their targets. It’s possible the Chancellor will do more with borrowing and less with tax than people expect.

Rachel Reeves made some choices before the election. She said she would stick with the same approach to measuring debt as the government. She said she would not raise taxes on working people, and would not raise national insurance.

Will these pledges stand the test of time?

The government (like everyone) want to get growth going and investment up. But their seming solution - to borrow the money and have the government “invest” it - is unlikely to be good for growth.

There are lots of problems in government. If the government take the easy way out and just borrow lots more, then those problems won’t get fixed. And we will be heading into the massive demographic fiscal crunch with even higher debt and borrowing.

The Financial Times has a game here where you can try setting your own budget:

https://ig.ft.com/chancellor-game/

I managed to deliver a budget I was satisfied with on my fourth attempt, but it required raising income tax by 5p in the pound!

My budget raised day-to-day spending by £4bn per annum, raised investment by £27bn per annum, and raised taxes by £55bn per annum, taking them to the highest level ever as a share of GDP. So the gap between increased taxes and increased spending amounted to £24bn, and yet I only just balanced the budget. I assume the difference is accounted for by interest paid on the national debt?