We have to stop borrowing so much

Labour increased borrowing by 80% - here's what that's costing you

“I used to think that if there was reincarnation, I wanted to come back as the President, or the Pope, or as a .400 baseball hitter. But now I would want to come back as the bond market. You can intimidate everybody.”

-Clinton advisor James Carville, (Wall Street Journal, 25 February 1993)

“The markets will have to fall into line”

-Paula Barker MP (City Am, 12 May 2026)

“The yields on ten-year gilts gained 18 basis points on Friday, hitting 5.18 per cent, the highest level since 2008. The yield on 30-year bonds, which are more sensitive to political uncertainty, gained 19 basis points to 5.85 per cent, the highest level this century.”

-The Times, 15 May 2026

* * * * * * *

It’s costing the British government more to borrow money. Because government is paying a lot of debt interest, that means either less to spend on other things, or higher taxes for you.

The cost of borrowing rose across the world during 2022, and the era of really cheap borrowing for governments ended worldwide. You can see the UK-specific spike caused by Liz Truss’s catastrophic “mini-Budget”, and see how it then fell back under Rishi and Hunt.

Alarmingly, you can also see how borrowing costs for the UK have started to diverge up and away from the pack of similar countries since autumn 2024. And how that divergence seems to be getting bigger:

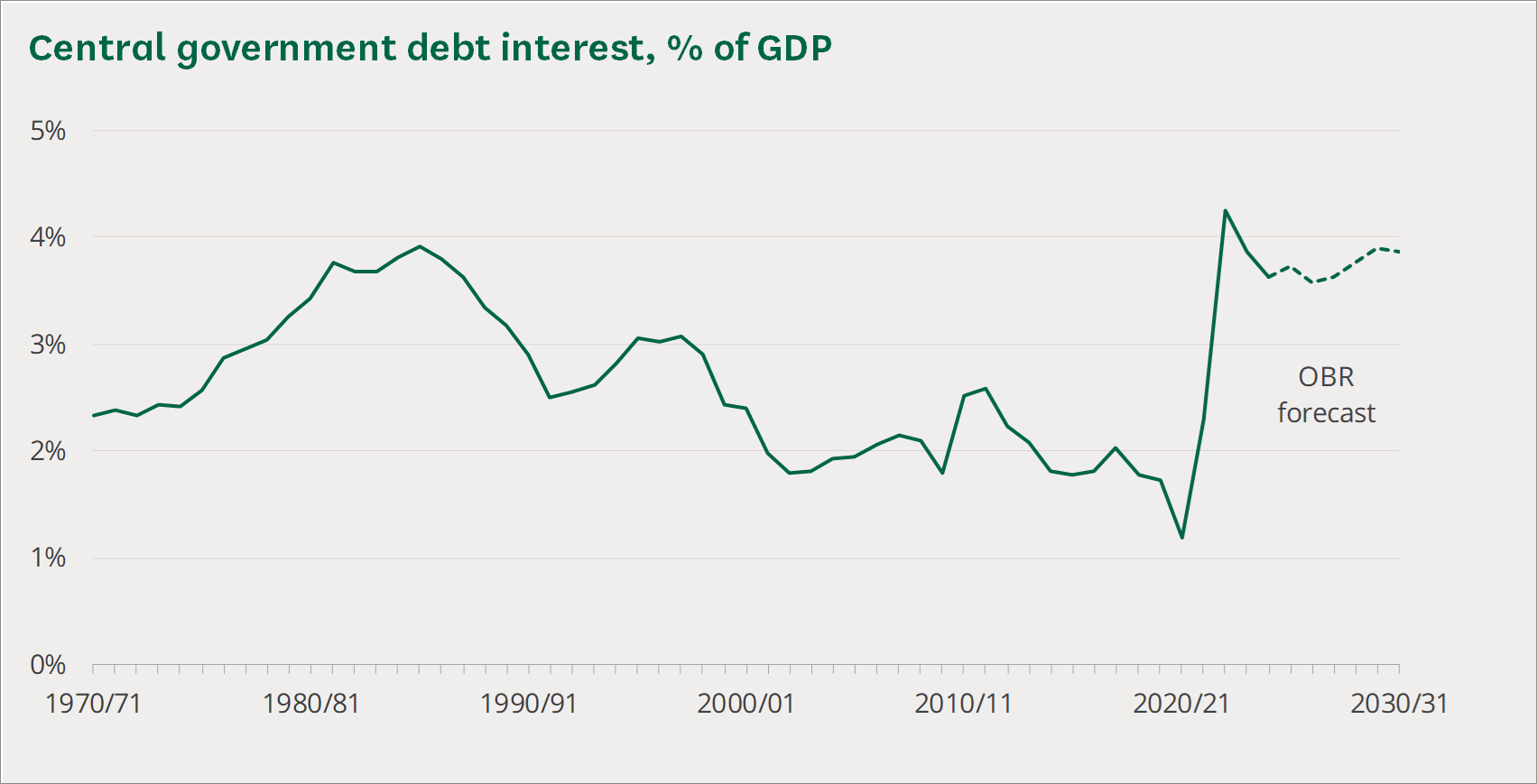

Higher borrowing costs1 mean that servicing our national debt takes up a larger chunk of public spending, and a larger chunk of GDP.

Here’s how much we spent on debt interest over time as a share of GDP. The cost fell back in the late 80s, again in the late 90s, and again during the 2010s. But now the falling trend has reversed.

We have gone from a bit under 2% of GDP to a bit under 4%. Even just that extra 2% GDP is a huge amount of money - about £65 billion a year. And for reasons I will get into below, I think even that gloomy forecast may be too optimistic.

What does the 4% GDP we are going to be spending on servicing debt cost you?

For example, if we were not spending this money on debt interest we could abolish all of the following: inheritance tax, business rates, capital gains tax, stamp duty on shares, stamp duty on houses, and fuel duty - and we’d still have money left over2.

The cost of the cost of borrowing

Obviously, we can’t just magic away the national debt. But even small differences to fiscal credibility - and therefore borrowing costs - make a big difference to taxpayers.

The OBR’s “Ready Reckoner” is that a 1% difference in gilt rates up or down changes spending by just under £10 billion a year by the end of the forecast.

As a bit of fun, here are the (very rough) sorts of magnitudes of things you could do if Britain had the same (lower) borrowing costs as some of our peers:

Same as the US. Even if we just closed the borrowing costs gap that has opened up between Britain and the US since 2024, that would be worth a lot. £5bn a year would let you raise the threshold for Inheritance Tax by about £150,000 - so from £325,000 to £475,000 or so, which would take a lot of people out of the tax altogether.

Same as France and Canada. If we could close the borrowing costs gap with places like France and Canada that’s about £10-15 bn a year. For context we spend about £20 billion a year on the police in England and Wales so we could have more than 50% more police if we could get borrowing rates down to French or Canadian levels.

Same as Germany. If you could get down to German rates that would mean £20 billion a year more to spend. With that we could cut the basic and higher rates of income tax by 2p, and give nearly 40 million people a meaningful tax cut.

How not to do it

One thing that pushes up gilt rates is fears of inflation - and Labour have stoked price rises with inflation-pushing pay increases in the public sector, Ed Miliband’s mad energy policies, and the disastrous Employment Bill.

But the main thing that drives borrowing rates, other things equal, are perceptions about whether a country has spending and borrowing under control.

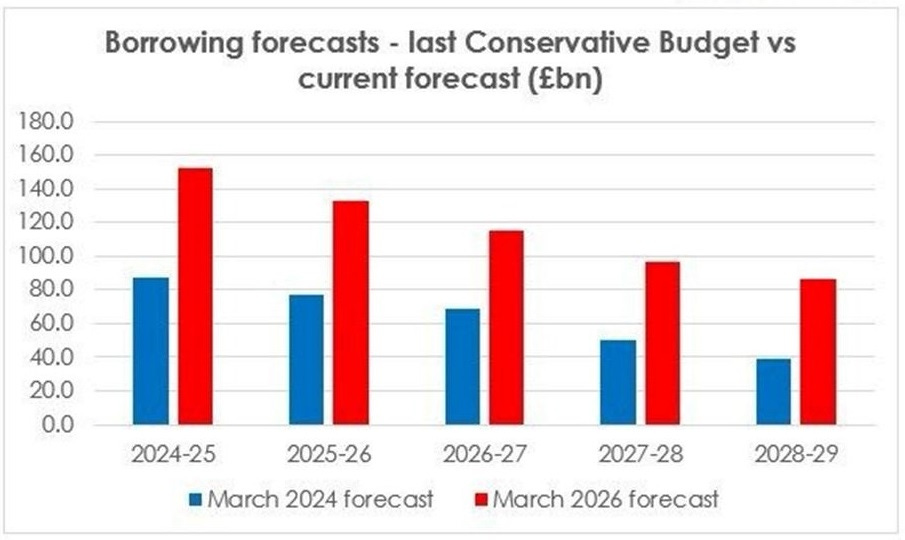

Under Reeves we are borrowing a lot more. Under the plans of the last Conservative government, we would have borrowed £323 billion over five years. Reeves is instead borrowing 80% more - £583 billion.

And even her plans for “deficit” reduction in the future turn on totally unspecified large spending cuts just before the next election.

Unsurprisingly, the IFS and OBR have been sceptical about this “plan”, and markets clearly share their scepticism.

And things are only going to get harder in future, as one of the main sectors buying gilts - the old DB pension schemes - is shrinking.

Right now markets are super jittery given world events. So what we really need to not do is stand out from the crowd as a risky place to put your money.

But we have a government that seems to be spending more and more, looks unstable and like it is about to embark on more reckless left-wing policies.

Recent rises in rates are directly attributable to the ongoing Labour leadership crisis:

Andy Burnham – the current favourite to replace Starmer – has criticised the government for being “in hock to the bond markets”, and to fund government spending “outside of the rules”.

Louise Haigh, an influential former cabinet minister, suggested weakening “the debt targets from the current three and five year rolling windows to a longer horizon of ten years”

Other Burnham outriders have variously suggested that bond markets will have to “fall in line”, or that “the British Parliament can’t be run at the behest of the bond markets”.

Whatever euphemisms or technical jargon politicians might prefer to use, this basically all means one thing: more borrowing.

In case you think I’m over-interpreting it, investors are openly saying this is what they are worried about.

Take this recent FT article:

UK borrowing costs hit their highest level since 2008 on Friday as traders priced in a greater likelihood that Andy Burnham would challenge Sir Keir Starmer for the Labour leadership […]

the UK was the worst-performing major bond market, which investors and analysts attributed to the growing political risks. “As an investor, my strategy is already [to be] short UK bonds and very short the pound,” said Adrian Owens, CIO for the Global Rates strategy at hedge fund group Investcorp-Tages. “On a Rayner or Burnham victory, we will be adding to both..” […]

“[The] market’s fear is that Burnham would be more left-leaning, and we could see [a] further increase in deficits,” said Mohit Kumar of Jefferies, who added that the bank was expecting this to weigh on sterling and longer-term UK government bonds.

And to compete in that leadership contest, we already have Starmer promising massive increases in spending, seemingly without any offsetting savings.

People always focus on the most extreme scenario: a fiscal crisis, in which ministers can’t control public spending, meaning they borrow more. Markets then lose faith in ministers and borrowing becomes more expensive, causing yet more spending in a positive feedback loop that ends with a visit from the IMF.

While we should never lose sight of this risk, a different risk is much more likely: the risk that we end up in a stagnant equilibrium with interest rates much higher than we should have, meaning taxpayer money is burned on unnecessary interest payments, meaning we end up with higher tax and lower productive investment, meaning lower growth, making it harder to serve our debt, keeping interest rates up and living standards down.

Conclusion: Money’s too tight to (not) mention

These growing risks, on top of the other economic problems that are piling up, are one reason why the Conservatives have set out a “Golden Rule” - that we will put half of all the savings we identify towards deficit reduction, rather than pledges to cut tax or spend money.

So at least half of the £47 billion of savings we set out last year would go towards deficit reduction. We are the only party making a clear, funded pledge to cut the deficit.

This is very unusual for an opposition at this point in the cycle - but we have just got to start talking about the deficit and debt again.

It’s boring, and in the era of dopamine-and-emotion-driven viral social media it is harder than ever to get people to focus on these boring-but-vital issues. The deficit never screamed at someone on TV, or went crazy in the street.

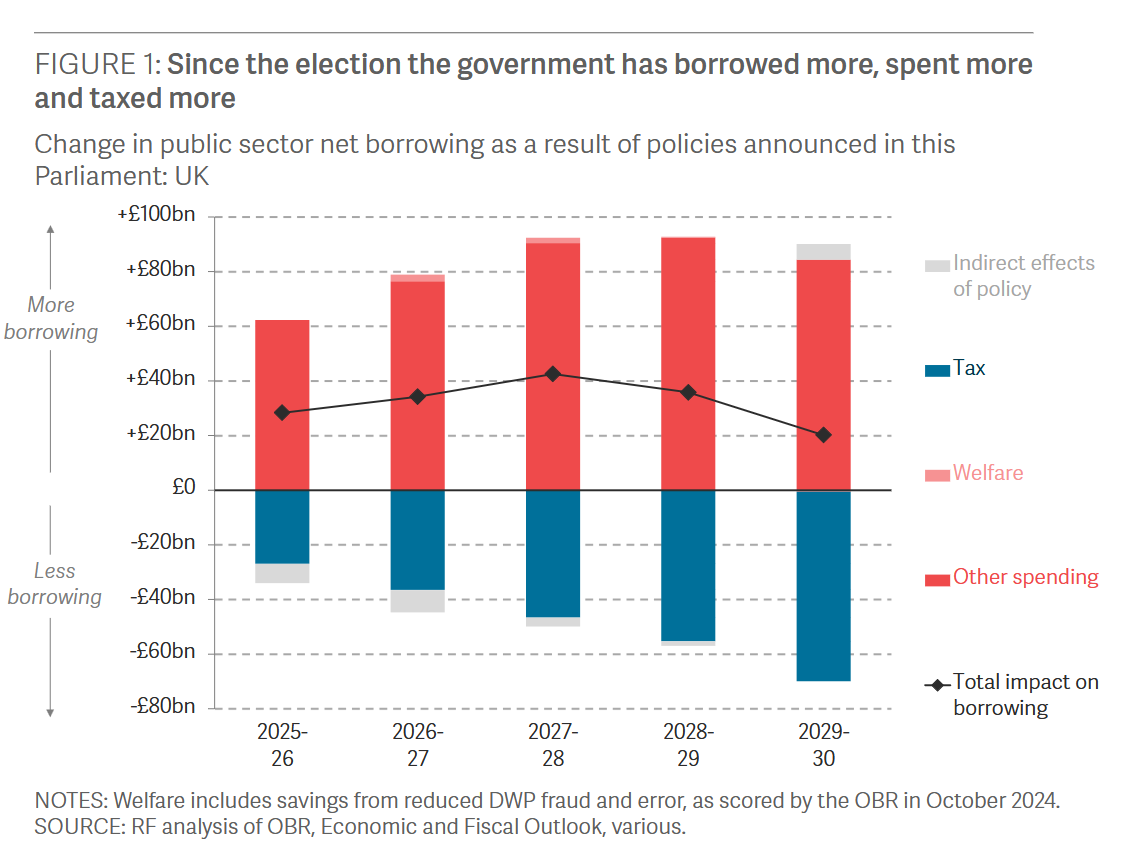

And yet, despite being boring, we have to focus on the deficit. Even the left-leaning Resolution Foundation published a report the other day which stated:

“The incoming Labour Government insisted it could transform growth and public services without reaching for “the tax lever”. In the event that lever was yanked, and yanked hard. Since the election the government has borrowed more, spent more and taxed more”

No kidding:

This mix of higher tax and higher borrowing is causing our borrowing costs to diverge upwards and away from our peers. That will have significant costs for taxpayers.

And that’s under Reeves and Starmer. Now we are about to embark on a Labour leadership race which is likely to be an auction of left-wing promises to spend more, with several of the contestants openly scornful of the idea that borrowing really matters.

As the opposition, we are trying to take the conversation in a very different direction.

But I have a bad feeling that under Labour we are going to learn the hard way that you can’t tell people you want to borrow from to just fall into line.

I fear things will get worse before they get better.

In simple terms, there are people out there who are willing to lend the government their money to finance public spending. Lending to the UK government, for historical reasons, is called a “gilt”, because the certificates used to have posh gold edges. It is essentially a loan where the investor gives the government a certain amount of money and that investor gets their money (the principal) back after a certain time (the maturity). Some have the size of the principal uprated in line with inflation to protect investors (index linked gilts).

As well as getting their money back, they also get paid a certain amount every 6 months (the coupon). Investors collectively have to decide what return (“yield”) they’re willing to accept to offset the risk of lending. If you don’t trust a government to pay you back in full or worry they will unleash surprise inflation on you, then you are likely to demand a higher yield.

See tables 3.1 and 4.1 of OBR EFO March 2026.

While this is all very worrying I have no faith in the conservatives to reign in spending and I get the impression that view is mainstream.

I'm good until the part where not serving the debt means more reduction in revenue. Makes no sense to me. Reducing the debt is probably impossible, but at minimum Herculean. Cutting any taxes will exacerbate the problem. It's the sort of Reaganite idea that got David Stockman fired.