Asset prices and fiscal fragility

Rachel Reeves is keeping her fingers crossed for fiscal drag on rapid asset price growth

Today the UK government’s borrowing costs hit 5.76% - the highest rate for 30-year debt since 1998. The increase in borrowing costs will drive up government borrowing costs, which will push up taxes further, other things equal.

The increase in our borrowing costs in the last month is a lot higher than in other developed countries.

The markets can see that Reeves’s forecasts are held together with a bunch of increasingly implausible assumptions.

For example, at Autumn Budget she inserted a random assumption that she will find £9 billion of totally unspecified “efficiency savings” over the last two years of the forecast. As the IFS noted drily: “governments have a clear tendency to promise future cuts which they don’t go on to deliver.”

The OBR produced a list of some of the other risks - for example, that a record tax-raising parliament might dampen growth more than she expects, and bring in less. They also noted risks “from industrial action in the NHS” and the plausibility of “the achievement of planned reductions in asylum accommodation costs by the Home Office”. That already looks very shaky.

The OBR noted that “A further risk is the future costs of welfare spending following the sharp growth of disability and health caseloads since the pandemic.” I have written about that before - given the government has been defeated by Labour backbenchers, they have no way to control welfare spending.

But one of the less well known bits of sellotape and string that are (just about) holding together Rachel Reeves’ fiscal forecasts together are some really optimistic forecasts for receipts from taxes on assets, based on a mix of tax increases and rosy assumptions about ever-rising asset prices.

But what if those rosy assumptions don’t work out?

Shaky foundations

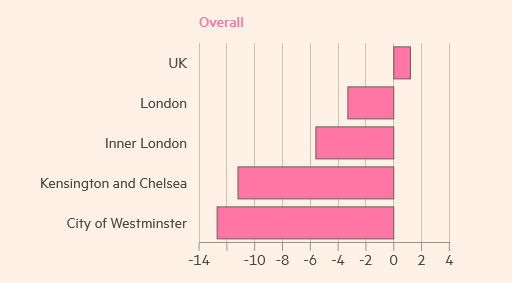

I have been mulling this for a while - and was reminded of the risk the other day by a story in the FT saying that house prices in central London were falling fast:

Prices are particularly down in the centre of the city:

Obviously, other things equal lower house prices would be good news for someone who wants to buy or rent.

But of course other things aren’t equal - and the outflow is being driven by problems with our economy and the fact that international investors are running for the hills:

You might not be sympathetic to investors - but falling asset prices might have a bad consequence for the public finances too, where the numbers are flattered by assumptions that asset taxes will yield lots of money. (This assumption is one reason the Conservatives’ plan to abolish stamp duty on the primary residence is not cheap.) Together Reeves hopes to have increased her takings from these taxes by over £35 billion by 2030.

Life’s a (fiscal) drag

At Spring Statement Reeves got a £5bn windfall from assumptions about CGT increasing, which helped offset some of the extra spending she has announced since the Autumn.

Some of the growth is from Reeves’ own tax increases (like the family farm tax and family business tax) - and some from an assumption that the assets she is taxing will keep on going up, while frozen thresholds for IHT and stamp duty drag more and more into paying. (This is “fiscal drag.”)

That’s why Reeves will be keeping her fingers crossed for increases in asset prices - if anything happens to them her numbers will start to unravel in a big way. This is a kind of “fiscal fragility”.

This isn’t just inflation - these taxes are also increasing as a share of GDP. Stamp duties have long been about 0.5% of GDP, but are going up about half that again to 0.77%. Having been in a range of 0.15 to 0.25% GDP over recent decades inheritance tax is forecast to increase to 0.40%1. The three taxes taken together will have gone up by about three quarters of a percent of GDP from 2024 to 2030/312.

What happens when the go-getters get up and go?

But the big caveat to all these rosy forecasts is that they rest so heavily on asset prices going up and up. If there are any big changes to asset prices Reeves will have yet another headache.

What might do that? I don’t know, we could have big tax rises that make investors leave, followed by a war in the Middle East?

It doesn’t take many people moving to blow a hole in these rosy forecasts, because these are highly concentrated taxes.

Take inheritance tax. It is a very geographically concentrated tax. I have been frustrated for a while that the statistics on it are so poor, so I made an FOI request.

From it, here is the share of payers and revenues by parliamentary constituency3. Here’s the share of payers, which is concentrated in the south:

And the here’s the share of the tax raised - which is even more concentrated - particularly in London:

The map doesn’t really do it justice, so here is a chart where we line up all the constituencies from those that pay the least, to those that pay the most.

It isn’t just inheritance tax that is so concentrated - similar things can be said for CGT and property transaction tax revenues - they are highly concentrated on a relatively small number of large payers. And lots of these people are wondering if they want to stay in the UK with Reeves as Chancellor.

Conclusion

Sure, there are bigger problems for Reeves. As I noted at the top, even pre-Iran she had lots of implausible things baked into her forecasts.

So this is just another risk to add to a long list. Reeves will no doubt blame Iran in her next Budget - and it is indeed hitting the world economy. But it was Reeves who made a choice to run all these risks and cross her fingers - to set off on a 100 mile journey with exactly 100 miles worth of petrol.

Assuming she would face nothing but plain sailing was naive. And there’s something odd about building your plans on getting tens of billions more from large investor types and then doing everything you can to drive them away.

Maybe things on the asset taxes will still turn out fine. It just strikes me that the growing reliance on asset-based taxes is building another new fragility into our public finances. Let’s hope we don’t find out the hard way that this turns out to have been a mistake.

Footnotes

To produce the forecasts for IHT the Treasury / OBR basically just uprate current numbers:

“Administrative data on a sample of estates are used to estimate the total population of estates being passed on at the point of liable deaths and the amount of tax due on those estates. The data are projected forward using our forecasts for things like house prices and equity prices.”

In a piece for the IFS in 2023 Arun Advani and David Sturrock use a more sophisticated model looking at the Wealth and Assets Survey to work out assets held by different generations approaching the end of their lives - they make the point that there is a boomer bulge underway - Reeves might hope that could offset problems with IHT.

I have labelled the chart “stamp duty” because people know what that is but this includes the equivalent Scottish and Welsh property transaction taxes.

The published stats by constituency are hopeless and don’t cover most constituencies. But I had to FOI to get this - the government refused to answer a perfectly simple parliamentary question twice. It’s absurd.

Thanks. Useful, hard to find, real UK fiscal information.

«You might not be sympathetic to investors - but falling asset prices might have a bad consequence for the public finances too, where the numbers are flattered by assumptions that asset taxes will yield lots of money.»

As usual an interesting post with interesting data, but this point amused me because if asset prices fail to rise for a significant period the least of the consequences will be lower taxes:

* If any asset fail to generate large capital gains and fat profits then a large part of "investors" will sell them as quickly as they can and then this will spiral into a crash.

* Assets are collateral for a colossal amount of debt as it is well known that over 90% of UK commercial bank loans are mortgages collateralised by asset valuations. The whole UK financial system could blow up like it did in 2008-2010 and it is by no means certain that any government could hand out to them many other hundreds of billions of free cash and 0% "loans" to bail them out again without causing major troubles.

* Most importantly rising asset prices are the core electoral base of thatcherism/blairism: most of "Middle England" is still made by workers and those workers will only vote for lower labor costs if they get large capital gain and rents from property that more than compensate them.

As to the latter point up to 2021 the Conservatives were unusually winning commons by-elections while being in office thanks to the huge property gains post-COVID and they only switched away from Conservatives when property prices went flat in 2022 and switched away from New Labour as they stayed flat to this day.

Since Thatcher and Blair every english general election is a property price referendum and if asset prices do not rise “fiscal fragility” will be the least of the worries for whoever is in office.