The great rail fares mystery

How much should a train ticket cost? On Britain's railways there's little consistency to how this question is answered.

What explains the price of a given railway ticket?

Obviously, it’s related to how far you are going to travel.

But it’s also… kinda not.

For example, the map below shows the price per mile of a weekly travelcard to London.

This is the exact same kind of ticket from each place. It’s generally higher for shorter journeys, but there are also massive differences between places that are similar distances from London.

Why is a travelcard from East Grinstead (£82.90) nearly half the price of one from Tunbridge Wells (£145.70), despite commuters travelling similar distances, on similarly packed commuter trains?

Why does it cost twice as much per mile from Swindon (£4.03 a mile) compared to Grantham? (£1.99 a mile.) Why are people in Leicester paying nearly twice as much per mile (£3.42) as people in Kings Lynn (£1.84)?

Given these big variations (which are also reflected in the prices of longer-term season tickets) it is no wonder that commuters in some places feel unfairly treated.

And if you look at other types of ticket the variation gets even greater and harder to explain.

Comparisons are tricky: there are open returns, and specific day returns for peak, off peak and super off peak. Then there are advance tickets for specific trains and other more exotic options like carnets... and so on.

But even if we only venture a little way into this jungle of prices the variation is even greater than for season tickets, and has even less of an obvious rationale. The map below compares the price per mile for either an Anytime Day Return or an Open Return - whichever is available and/or cheapest.

There are clear patterns. How come journeys out along the Essex coast, or up to Cambridge or Kings Lynn are so much cheaper per mile than trips to the South West or North West, or up the Midland Mainline? Is this really the “market” in operation? Or something else?

I know operators do change their prices in response to demand and crowding a bit. But does this really explain the difference? Sure, Paddington and Euston and St Pancras are pretty rammed - but then so are Liverpool Street, Kings Cross and Fenchurch Street.

Is there really some difference in demand versus the cost of supply that can explain such big differences in price? If so I would love to hear from commenters.

In some cases I can see an explanation up to a point. It costs twice as much from Cardiff (£3.01) as Liverpool (£1.53) on a travelcard if you take the slower operator.

But in many cases where there’s a similar service the prices are radically different.

Adding to the complexity, many fares are just not even available in different places - for example for the map above there are 203 stations where Anytime Day Return fares are available, 111 places where you can get an Open Return which lasts a month, and 16 where you can get both12. If anyone knows why this is so I would be very interested: there doesn’t seem to be any obvious pattern.

There is also often not much difference between the price of a return and a single, particularly where the price of the return is being held down by regulation and the single is not. As most people now know, you can often save money using a ticket splitting app and buying two or more tickets to get you from A to B. And many people who don’t have access to more than one operator feel like fares are cheaper where there’s competition.

All these factors and more have let to a pervasive feeling of distrust among rail passengers that the price they pay isn’t a fair one, and that they won’t even always get offered the best price unless they search quite hard.

How did we get here?

Under British Rail fares the price per mile already varied quite a bit, including for historic reasons. When big investments were made and services improved, the Treasury would get back its pound of flesh by increasing prices. I’m told this happened after electrification of the East Coast Mainline in the late eighties.

At the point of privatisation in the mid nineties these differentials were partly baked in.

Governments of all colours have taken a (very) mixed approach over recent decades. On the one hand they want to encourage some degree of market forces, and to let operators set fares.

On the other hand, about 45% of fares are regulated. Typically commuter fares such as season tickets and shorter distance peak singles and returns are regulated.

There is a feeling commuters are a captive market, enjoying no real competition. And if you immediately shifted to charging whatever the market would bear many people would just be unable to afford it - though the result would be a commuter riot and the overthrow of the government long before you got there.

Longer-distance off peak singles and returns are also regulated, along with anytime fares around the main cities. First Class and advance fares are much less regulated. Within London there’s a whole other system.

For those fares that are regulated the government announces each December what the average increase will be, and there’s a huge amount of politics around this. Last year the government announced a substantially below inflation rise, but most of the time since the 1990s overall fares have risen by more than RPI.

From the 1990s to the middle of the last decade government also set a “flex”. Operators were able to grow their from regulated fares in line with a particular increase (say RPI +1) but within their overall basket of fares were allowed to grow some fares faster and some slower. While this meant fares became more market-oriented, it also meant some people got really big increases, and for this reason the flex was then abolished.

I am not enough of an expert to know whether the flex would have meant that patterns of pricing would have meaningfully converged toward “market” rates - whatever that might mean.

As a result of these processes some broad trends in prices for types of journeys are visible.

Regulated standard fares are two and a half times the price they were in 1995 (slightly below RPI), while unregulated standard tickets are three times the price, and first class tickets are four times the price.

Until the 2010s long distance fares increased more than regional or south east commuter fares, though they have increased at similar rates since.

Rail fares had grown faster than inflation but recent decisions to hold them down below recent (high) inflation have unwound that. In fact compared to 1995 regulated standard fares have now grown by less than RPI and all standard fares by not much more than RPI.

Here is the same data two ways. First a nominal index:

And now real:

So the answer to the question at the top - what explains current ticket prices? - is some combination of historic prices, and flexibility within and outside the regulated fare system.

This explains how fares got to where they are - but are the resulting prices sensible, or at least moving that way?

What should rail tickets cost? Couldn’t we just pump in more subsidy to cut the high prices?

How much should rail tickets in general cost? “Much less”, would be the answer of most regular rail users. But a taxpayer who doesn’t use the railway much might take a different view. In 2022/23 the taxpayer spent £11.9 billion subsidising the running of the railway - the equivalent of roughly 2p on the basic rate of income tax. In total the taxpayer spent over £20 billion, including funding for enhancements.

The cost of the running of the railway would probably have been a little lower if not for the pandemic reducing passenger numbers. But it would probably not have been that much lower, given the previous trends3. This is why there is such a strong reaction to old-school practices and pay deals that make the railway even more expensive to run.

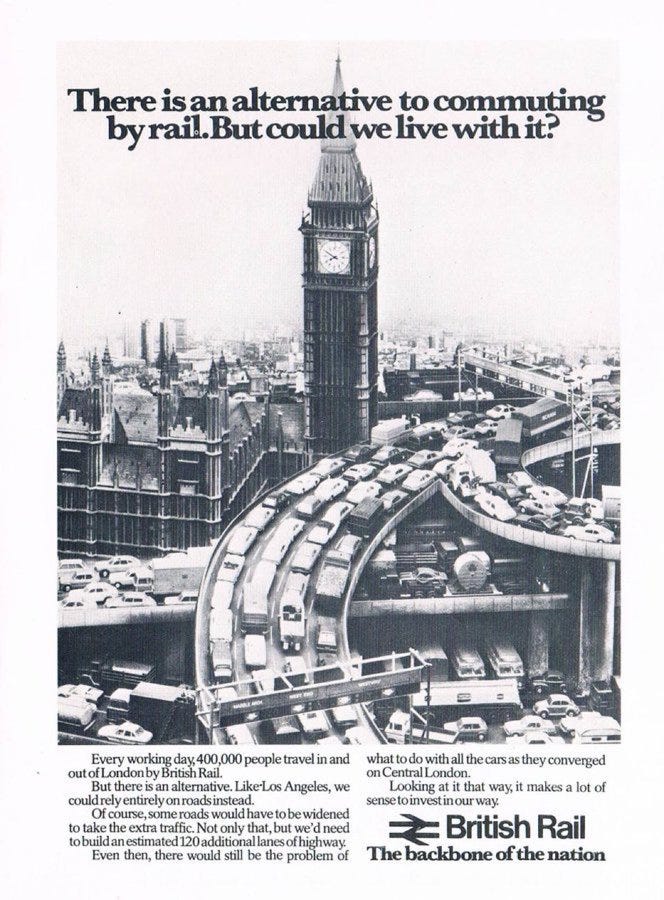

Rail advocates call for more subsidy on the grounds that rail is green; that roads are subsidised, that rail can unlock both housing growth and agglomeration gains, that its a nice way to travel, and that the alternatives are implausible because a rail line can move so many more people than a road. This last one is a long-running line of argument, as the late 1970s poster below suggests:

Critics would say that road has only a tiny fraction of the gross subsidy per mile of rail - and even this is more than paid for by Fuel Duty and VED receipts; that road travel is now going electric and that much of the rail network is still not; and that rail (even including the tube) is only about an eighth of all travel by passenger miles - so we will generally get much more bang for our transport buck by improving roads instead.

Who has won the argument? Well, in practice government subsidy to the railways has been increasing in real terms over time.

And a fair price for a ticket is only one thing that rail users are looking for. They want to avoid overcrowding and standing; and have a reliable and modern service. The price of the ticket has a major impact on crowding, and by contributing to revenues it also partly funds a better service.

So for all these reasons I don’t know whether route to lower fares is likely to come from a further large increase in subsidy. Is there a way to do things better - including reforming fares?

Reforming rail fares

There have been several rounds of reforms to fares. The coalition government produced a review in 2013 which looked at all the different priorities. Its main thrust was to push digitisation of tickets. But it also argued for a reduction in the ‘flex’ that was causing the largest large fare increases, and also for the creation of more flexible tickets - which led on to later innovations like part-time season tickets. Government and industry were gearing up for another big push in 2019, but the process was sideswiped by the pandemic.

Nonetheless, things are happening. The industry this year presented another vision document. I think there is a case to go way further on flexible tickets - the current “part time season ticket” covers far too few journeys and the join up with other modes of travel in the cities still has a long way to go despite recent progress (spurred also by the MCAs and 2017 Bus Services Act).

One frustration for me is the inability to get a travelcard that includes the London Underground without getting a paper ticket. That’s because digital rail tickets use QR codes, while the much of the tube can use only RFID (like Oyster) or old paper magstripe tickets. This feels like it should be solvable. My local operator (East Midlands) have also withdrawn the option to buy “carnet” tickets unless you travel first class, which is annoying.

Last year LNER moved onto a trial system of “single leg pricing” which is supposed to be simpler; to end the strange situation in which returns are similar price to singles, and better fit pricing to patterns of demand. But while the move to single leg pricing seems very sensible, there has been a lot of complaint about the removal of super off peak fares, which removes a cheap option for people who walk up in quieter periods.

Despite these other changes, I can’t get away from those maps at the top. There seem to be pretty big differences in pricing, and I can’t see any obvious reason they reflect either “market forces” on the one hand, or any kind of logical or fair arrangement on the other.

Perhaps someone can explain in the comments!

The map shows the cheaper of the two where both are available. Because LNER is moving onto all single leg tickets, prices on the East Coast mainline reflect returns available from other operators on this route like Lumo.

Both of the maps above may be unfair comparisons, and they are definitely incomplete - to get a sense of the totality of how much people are paying to get to London from these different places you would need to know how many people are travelling on all the different types of fares. And even then there is a circularity: when and how many people travel is partly determined by the fares.

Here’s the trend on operational spending and passenger revenue over recent years from ORR Rail Industry Finances:

MANY thanks to Jamie Broom for the data crunching for the maps in this piece.

The differential in fares is in many cases a result of the former Network SouthEast vs Intercity categories on BR. As separate divisions fares were set separately, with a sometimes significant differential to reflect the then much higher quality of 'Intercity' services vs commuter NSE ones.

Kings Lynn in particular was the farthest-flung reach of the old Network SouthEast area. Conversely, on the Midland Main Line, the boundary is very close to London at Bedford.

Compare the colour of the dots with what is now called the Network Railcard area - it matches the discontinuities almost perfectly.

The unevenness in South Essex between what are now GA and c2c has also been the case for about a century now. Basically, the Great Eastern has always been the faster, more prestigious line, whilst the LT&S was a working class suburban railway, so fares developed in line with this.

Switzerland 🇨🇭 (STATE OWNED) is Europe’s most reliable rail system, with 92–94 % punctuality and a dense, integrated network. Fares are around €0.22/km (≈ £0.19/km) and roughly half the costs are covered by subsidies (≈ CHF 5–6 bn/year). Spain 🇪🇸 operates Europe’s largest high‑speed network (about 4 000 km) and offers 300–310 km/h trains run by RENFE (STATE) and other operators; competition keeps fares down to about €0.10–0.12/km (≈ £0.09–0.10/km) with a moderate €1.4–1.6 bn annual subsidy (≈ 25–30 %). By contrast, the United Kingdom 🇬🇧 (PRIVATE) has some high‑speed routes but remains Europe’s most expensive rail network at about €0.35–0.40/km (≈ £0.30–0.35/km) despite £11.9 bn in public subsidy; infrastructure is public but train services are run by PRIVATE FRANCHISES, and punctuality lags behind continental peers at 75–80 %.