British energy policy part 2: accelerating towards deindustrialisation and disaster

The previous post looked at how the UK has seen falling energy use, partly driven by expensive energy - which in turn has been driven by an unprecedented dash for renewables - even as the wider world continues to add cheap fossil power.

In this post I want to address why the cost may well increase dramatically as part of Ed Miliband’s dash for a zero carbon grid by 2030 - and why that is likely to have disastrous consequences.

* * * * * *

Running up the hellslide

At the soft play centre our children quite like the hellslide. You may remember them: big tall slides that are shallow at the bottom but almost vertical at the top, causing little squidgy infant-school children to acelerate to the speed of sound on the way down.

Ed Milliband is driving towards a zero carbon grid by 2030. What Miliband wants to do is rather like running up the hellslide, because the path he wants to take us on gets radically steeper, or rather, more expensive.

Labour’s March 2024 energy paper promised to

“Quadruple offshore wind with an ambition of 55 GW by 2030

Pioneer floating offshore wind, by fast-tracking at least 5 GW of capacity

More than triple solar power to 50 GW

More than double our onshore wind capacity to 35 GW”

Now, on the face of it a zero carbon grid by 2030 looks very very hard, but not totally insane.

In 2023 about 38.5% of our electricity came from fossil sources. And over the decade 2013-2023 wind, solar and hydro went from 8.5% to just over 33.5% of our generation - up 25%. So at the same pace (the fastest in the world) you might think we can be carbon free within 15 years or so - taking you to 2038.

And the industry rumour is that “net” zero electricity will be defined by the government as meaning something like 95% carbon free, and that in itself would shave two years off the timeline in the paragraph above.

So couldn’t we just close the remaining gap to net zero electricity in 2030 by… doubling the pace of deployment or something?

There are two problems. First, many people question where all the people, kit and highly specialised ships are going to come from to go even faster. As we discovered during the sprint for rail electrification after 2011, there are often serious bottlenecks when you try to get more of a lot of specialised engineering done really fast.

But there’s actually an even worse problem that makes the hellslide steeper still. To date we have been adding a relatively small amount of renewables to a mainly fossil-fueled grid. When the wind doesn’t blow, we just turn up the gas. The figures quoted above for capacity don’t tell the full story. You can have a lot of solar or wind capacity but if the wind drops or the sun doesn’t shine, you don’t have any actual power.

There is already a cost to the intermittency of renewables of course: we pay wind producers bonus payments not to produce when it is very windy, and gas producers get extra to throttle up on demand: CGTs are physically much less efficient if you run them in this stop-start way to balance out intermittent renewables. The costs of balancing the grid have already increased a lot, from £1bn in 2018 to £4.2 billion in 2023 - equivalent to £150 per household.

One of the problems is that the producers of intermittent power do not pay the price of their intermittency: this is something which the Helm Review said should be fixed, but which has not been properly addressed.

But at the moment we can still rely on gas to throttle up and down, which it does rapidly. As an example, the chart below shows how we got our power during January 2024. Wind output bounced around between 2,900 and 16,000 MW. Pumped storage and interconnectors took up some of the slack when it wasn’t blowing, but ultimately we relied on gas (in orange below) to very quickly throttle up and down between 2,000 and 26,000 MW to meet the daily peaks of use.

Could it be magic?

If you don’t have that controllable gas any more you need to massively overbuild renewables so you aren’t short that often, and then have enough left over to also fill up some kind of new storage system. You need far more capacity than you will use on average, and then lots of storage too, but at present that is very limited and expensive.

This is where magical thinking kicks in. The plan only really works if you assume some magic new storage technologies.

James McSweeney has an excellent walkthrough of why Ed’s plan will fail. To avoid blackouts it would rely on the rapid creation of a huge amount of energy storage, which will only be economically feasible with technologies which don’t currently exist.

Brian Leyland also looks at this, concluding that wind power would need battery storage costing 80 times more than the cost of the wind farm, even if sufficient battery capacity was available (which it isn’t).

And there are other reasons why the challenge is likely to get harder too:

Ed Miliband also wants to decarbonise other sectors by shifting them onto electricity - like domestic heating, so we will need lots more electricity.

To date, the pressure has been taken off gas a a bit by the remaining baseload: a residual bit of coal (which ended this week) nuclear (almost all due to shut soon) and a lot of biomass. Both these latter sources have problems.

Miliband has talked about extending the life of the 8 out 9 reactors that are due to shut by 2030, but so far nothing has happened, and it’s all gone quiet post election. HMT has successfully strangled new nuclear for my whole lifetime, so it remains to be seen if anything will really change. Even if it does, the renaissance in nuclear generation will come a long time after 2030.

People have increasingly clocked that transporting a load of heavy wood from Canada in ships which burn (tar-like) bunker fuel emits more Co2 than coal and may have a net negative effect on the climate. Emissions at the smokestack are four times that of coal, and very dirty. No-one disputes that it will certainly increase emissions over the lifetime of me and my children - and it is very likely to raise them even if the forests we are burning are allowed to grow back. It is very expensive greenwash, and at some point people are going to want to get rid of it.

Take away these sources of baseload and things get harder.

A lot of the renewables that are being added are in places like the north of Scotland and north sea) which are a long way from the demand. The current grid is designed around a bunch of big power stations in the industrial Midlands and Yorkshire, so we will need to totally rebuild the grid within just a couple of years.

Won’t new technology make renewables cheaper though? You would hope so, but there are factors pushing in the other direction.

You naturaly put renewables on the best and cheapest sites first, so tend to end up with more difficult or expensive ones over time - deeper seas, more expensive and less windy land. Capital costs, operating costs and equipment costs don’t seem to be going down in the way people hoped.

Solar technology really has improved, but sadly this doesn’t help much in the UK, as it produces so little electricity at the point the UK really needs it - in the middle of winter.

If you are Texas, with large hot deserts with negligible land prices, and your demand for power peaks in the middle of the day in the summer (because of air conditioning), then solar is great news.

In the UK, where demand peaks in winter, land is expensive and we have quite a bit less sunshine, then it won’t do much. For example, in December last year year solar produced energy only between 8:30 and 3:30. Over the month as a whole it provided 0.85% of our power - with massive variability from day to day. A World Bank report on solar potential suggests that while it will be a game changer for countries like Namibia, Britain’s potential for economically doable solar is lower than any other country other than Ireland.

Where people already own the land (roofs of buildings, car parks) solar is much cheaper and a good deal. But solar farms for industrial production are not cheap, because land isn’t.

Some people think the smart grid can solve all this, and I’m sure it can help in the longer term. One popular idea is that we will all have electric cars and bidirectional chargers, allowing the grid to charge your car at night with more power than you need to get to work, and then discharge during the daily peak, so the grid will get a load of battery storage for ‘free’. But at present only 3.5% of cars are fully electric and even within that the proportion of charging points where there is infrastructure for bidirectional flows seems tiny. The government says it has funded 500 bidirectional chargers, and is funding experiments in this area. This tech sounds like it will help in 2050, but it won’t help much in 60 months time.

While Ed Miliband will not succeed in getting to a zero carbon grid by 2030, the costs of the attempt will likely be with us for years to come: attempts to further rapidly jack up the share of intermittent renewables will likely require very expensive storage which will cause their costs to accelerate dramatically if we are not to risk shortages. This will not just have a transformative impact on the physical landscape, but do irreversible damage to our industrial landscape.

What about nuclear?

What’s the alternative to Miliband’s plan? As well as going more slowly and aiming to match our efforts more closely with others, one way to do things differently is to shift the emphasis from renewables and batteries to nuclear.

At the moment eight out of nine UK reactors are going to shut by 2030, so it is falling away not growing. We should extend their life and the government says it will do this and press on with the two nuclear projects currently underway. But there is a strong case that doing more with nuclear rather than all renewables and storage would be cheaper over the coming decades.

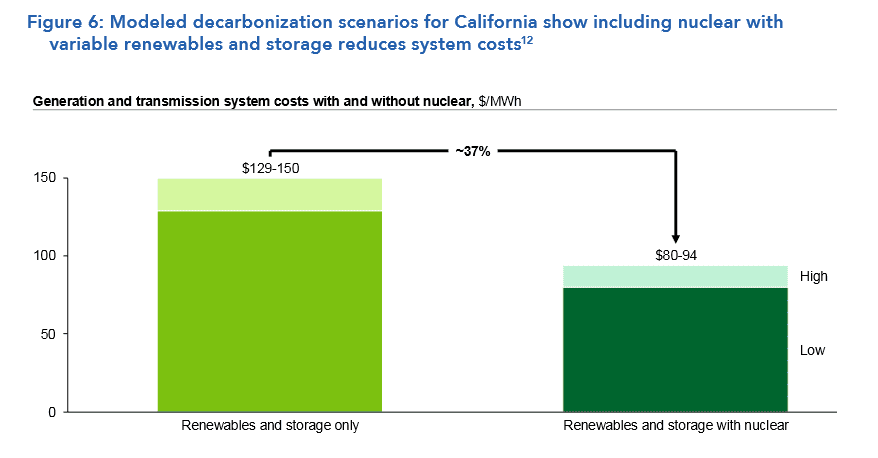

The US Department of Energy produced a major report this week, the conclusion of which are strongly pro-nuclear. It argues (based on a previous study of California) that having a big slug of nuclear in the mix reduces costs per MWh by more than a third compared to an approach based on just renewables and storage:

Seperately, the Biden administration announced that it would contribute $1.5 billion to the first ever reopening of a nuclear power station in Michigan.

The report is a sophisticated walk through the complex arguments, and notes that amongst other things:

“decarbonizing the grid will be very difficult and expensive without 20-40% clean firm power… Nuclear consumes 11-38% the mass of critical materials per GWh than solar, wind, and battery technologies… nuclear power may have lower transmission requirements… Many of the most energy-intensive industries also rely on uninterrupted, high-pressure steam, for which nuclear is among the few alternatives to fossil fuels…”

Directly comparing the cost of nuclear to individual fossil fuels or renewables is not straightforward. A concept called Levellised Cost of Energy (LCOE) is sometimes used, but as David Turver explains here, this is highly sensitive to discount rate assumptions. The approach struggles to capture the benefits of long- lasting assets like nuclear power plants. The DoE report says that

“Levelized cost of electricity (LCOE) does not capture the full benefits of nuclear as a clean firm resource. These include the value of an 80-year operating asset, the value of firm generation to provide power during key periods of grid need or when other variable resources are not generating, and the value of clean electricity relative to carbon emitting resources. LCOE also does not fully account for the value of reliable, carbon-free heat for industrial steam, which is critical to many industrial processes and has few decarbonized alternatives.”

Like many other studies the DoE report notes the importance of “learning by doing” and scale for nuclear. Where countries build simple boring nuclear at scale (like France from the 70s to the 90s, or South Korea recently) the costs are pretty reasonable, and you are buying firm power. If instead you build expensive one-off plants with idiosyncratic technologies as the UK fitfully has, you jack up the costs.

Britain Remade have compared the costs, and explain why they have escalated over time. Things like the ALARA principle have also led to goldplating. For example Hinkley Point C has special intakes to avoid fish being sucked in (unlike older stations) but in addition to that were made to include underwater sonic equipment to shoo fish away (“Acoustic Fish Deterrents,” also known as the “fish disco”).

With this in mind it is no mystery why British nuclear stopped being cheaper than coal.

Nuclear is not quick to build, as Nick Clegg pointed out in his infamous clip. But then again several offshore windfarms have taken just as long to deliver - they aren’t quick either. All the more reason to get on with it now.

4) Energy use is strongly linked to growth

As noted in the previous post, our emphasis has been on driving down domestic emissions - but we have done this partly by using high prices, which has encouraged industry to locate in more polluting locations from which we then import goods.

Making the Climate Change Act a legal requirement and setting Carbon Budgets for short periods makes the focus of policy incredibly narrow, short term and legalistic. Ministers frequently get submissions saying they legally MUST do policy X or Y now because it can make some carbon saving (regardless of cost or strategic purpose).

Above all, our framework is totally focussed on reducing UK domestic emissions (0.77% world emissions) rather than our contribution to developing the technologies that can solve the global problem.

If you adjust for the energy embedded in imports (so called consumption emissions) the “embodied emissions” in the stuff we import account for a bigger share of total energy use than in any other major industrial economy. In 2019 embodied emissions were 25% of the total in the UK, compared to 12% in the US, 11% in Germany and 3% in Japan.

Let’s look at what that has meant for some energy-intensive industries already.

Take steel. Between 2000 and 2023 global production rose 123%. But production in the UK fell 63%. Our share of world production is less than a fifth of what it was in 2000, down from 1.8 to 0.3% of the total. China more than tripled its share, India more than doubled it and even other old industrial countries did better: Japan has 37% of its 2000 share, the US 36%, Italy 35% Germany 34%, Canada 33%, France, 21% and the UK just 17%. We are the biggest loser in the G7.

Even in the UK, which is growing much more slowly than the world, the demand for steel hasn’t gone away: it’s just that we now get more of it from overseas. We now import about £2 billion a year more steel than we export. And this is before the shutdown of blast furnaces and virgin steelmaking in Port Talbot and Scunthorpe.

You might think that something like cement, which is has a very high weight-to-price ratio, wouldn’t suffer the same competition from high-carbon, cheap- energy countries. But in May the industry warned that about 40% of the market was now captured by imports from high carbon-intensity countries, up from 10% in 2005. The Times quoted one of the players in the industry:

“We want to invest in the decarbonisation of the industry,” Simon Willis, 58, the chief executive of Heidelberg Materials UK, said, citing delayed plans to introduce carbon capture technology at its Padeswood plant in north Wales. “If the country wants to offshore its carbon [by relying on imports], then the alternative is de-industrialisation.”

Production is also now falling - the UK produced about a quarter more cement in 2019 than it did in 2023.

The same things are happening in refining. The UK has gone from having 18 refineries in the 1970s to six now - soon to be five when Grangemouth shuts and is turned into an import terminal. Between 2011 and 2023 production of petroleum products fell by just under a third.

These kinds of energy intensive industries have taken a pounding already, with output falling massively, and declining even compared to other manufacturing.

There is a strong link between economic growth and energy use globally. Here is electricity production. With the exception of gambling hubs like Macao (the dot in the bottom right), there are almost no rich countries that don’t have high electricity use - and vice versa.

The UK has experienced unusually intense deindustrialisation. Our share of world merchandise trade has shrunk more than most other countries.

In general there is a strong link between changes in electricity production and changes in countries share of world merchandise trade. With a couple of exceptions in Eastern Europe, (where there was lots of scope to replace ineffecient communist-era production facilities) the countries that saw falling electricity output also saw their share of world merchandise trade shrink.

There has been a certain amount of scope for countries to cut electricity use with newer technologies. But in the case of the UK the reduction in consumption also simply reflects energy intensive industries leaving the UK for other locations (or not coming here) due in part to the UK’s unusually high energy prices.

Pinching where it hurts

The cost of decarbonising in the way we have has particularly impacted the poorer parts of the UK, which are more industrial. Fuel and environmental duties are skewed towards poorer regions because of different transport patterns and more industrial economies in poorer areas.

As a share of GDP, environmental levies on business are between a third and half lower in London (0.48%) than in more industrialised places like Scotland (0.99%) and the East Midlands (0.79%). The production and manufacturing industries most hit by the cost of going green are a much bigger share of the economy in poorer parts of Britain outside the south-eastern core around London:

And not only is manufacturing in concentrated in some places, but productivity growth in manufacturing has generally been higher than in the wider economy over recent decades.

These two things multiply together to mean that manufacturing accounts for a massive chunk of productivity growth in Britain’s poorer regions. For example, for the West Midlands, manufacturing accounted for about half of productivity growth from 1998 to 2017.

Our current approach - expensive energy to cut energy use - is extremely bad for such sectors and places.

* * * * * Is the future really low energy?

You might read the above and think that these production industries are high productivity, but still think energy intensive industries are thing of the past in Britain. In the 1990s there was a trope that argued that the future for advanced economies was one of lower energy consumption: that China would make the basics while we did the clever stuff in offices and design studios. Now that trope is itself a thing of the past. It turned out that making and designing are intimately linked, and China has rapidly come to be the main competitor to the US in frontier sectors in tech and AI, leaving Europe in its wake.

But now another nail has been driven into the 90s narrative - in the last couple of years it has become apparent that AI is doing to create a further huge demand for electricity on top of other things like electric cars and electric heating. An AI powered internet search uses ten times more energy than a normal one. The frenzied race for electricity in the US right now is further reason to think we should be aiming for energy abundance, not a low energy future. The following press snippets tell the story:

“Big Tech’s Latest Obsession Is Finding Enough Energy: AI boom is fueling an insatiable appetite for electricity.” Wall Street Journal, 24 March 2024

“A nuclear reactor at the notorious Three Mile Island site in Pennsylvania is to be activated for the first time in five years after its owners, Constellation Energy, struck a deal to provide power to Microsoft’s proliferating artificial intelligence operations.” (Guardian, 20 September 2024)

“The AI revolution is expected to more than double data centre electricity needs by 2030… data centres account for 3.5% of US electricity consumption today, and data centre electricity use could be above 5.5% in 2027 and more than 9% by 2030.” (Barclays Investment Bank, 24 August 2024)

U.S. electric utilities predict a tidal wave of new demand from data centers powering technology like generative AI, with some power companies projecting electricity sales growth several times higher than estimates just months earlier. (Reuters, 10 April 2024)

What should we do about it?

There are two questions, one bigger than the other

First, was the Helm Review correct that we could reduced emmissions at a lower cost, and how could we do this?

I think it is pretty clear we could do things more cheaply. We used to have normally priced electricity, now it is the most expensive - even in Europe.

Instead, we could have been - and still could be - more like France. If we build a big slug of nuclear that is likely to be a cheaper and less risky way to decarbonise than creating a grid that is incredibly dependent on intermittent wind and as-yet-non-existent storage technologies. Yes, there are lots of smart things we can also do at the margin to make the grid smarter and iron out peaks in demand. But we would be foolish to bet the farm on this.

The second, bigger question is how much are we prepared to pay to decarbonise.

The British economy reminds me of the heavily-laden donkeys I saw when walking up in Nepal. We have loaded up our little economy with many different demands. We want to spend on being a world leader in aid and defence and public services and to cut the cost of living. The demand to be a world leader in paying to decarbonise is just one of many demands loaded onto the back of this poor old donkey.

In the context of an ageing society something’s got to give. At present the UK plans to cut emissions (compared to 1990) by 68% by 2030, which is more than the EU, Japan or the United States.

Do we want to be ahead of the pack, rather than in it? There is a cost to this and is is two fold. First, there is a direct cost in terms of a higher cost of energy, which is spread widely through society.

But there is also a second cost in terms of lost competitiveness. For example, China is currently crushing western carmakers. Unless several big things change -including, but not limited to energy - then the future is likely to belong to them.

The costs of being ahead of the pack are likely to be non-linear:

1) If we add lots more intermittent renewables very quickly we are likely to run into much higher costs than a slower pace, including costs we haven’t had to face up to so far, because we have gas to balance the grid.

2) If you are a way out ahead of the pack in terms of energy costs you lose competitiveness. The nature of markets is non linear - if you are marginally more expensive you can lose not just a marginal share, but your whole business.

The logic we have been following is wrong - others countries that are booming are not following our dramatic, world-leading decarbonisation path. Much of Europe is in nearly as bad a position as us, and Germany is being brutally deindustrialised by the cost of energy. But Europe is no longer the world.

US decarbonisation has been largely about sewitching from coal to suddenly abundent natural gas plus improving solar. The US sees its role in inventing the energy technologies of the future, not sacrificing its future.

While we make sacrifices to be “world leaders” we are enabling China and and other countries outside Europe increasingly to dominate the future.

Energy is not the only part of the story here, but allowing them to add masses of cheap polluting coal to push down prices while making our own energy expensive has given them a massive advantage.

745 million people still don’t have access to electricity, and billions more who do are desperately poor. As long as fossil fuels are marginally cheaper they will use them.

Sure, some improvements in technology come from learning-by-doing and by rolling out existing technologies. But we have underemphasised the importance of investing in research into new technologies. The billions of people who have almost nothing just won’t pay more for energy.

We could get into carbon border taxes. The government promised a UK Carbon Border Adjustment Mechanism (CBAM) at the end of 2023, and the EU is planning the same. I don’t regard them as a ridiculous idea, but they are very limited in what they can do.

I don’t just mean that the UK plan omits certain very energy intensive sectors that are subject to a lot of international competition - like refining.

I don’t just mean that each component in each product from (different parts of) different countries will have a different carbon intensity. So it can never be neatly targetted.

Above all, while a border tax shelters domestic producers it doesn't help them as exporters, which is normally a key part of the output of firms in these trades sectors.

It makes others’ products a bit more expensive to match their higher costs in the UK (2% global GDP) but still doesn’t do anything about the fact we have made them uncompetitive in the rest of the world - the other 98%.

Globally its relevance is now very limited because our share of trade (and even Europe’s) is getting so small. To invert a certain charity single of the 1980s, we aren’t the world.

Conclusions

On the overall magnitude and pace of green policy we need a conversation about how much we want to spend on decarbonisation compared to all the other priorities we have - it is far from cheap. Choosing to be the decarbonisation leader, as at present, is likely to have additional costs from adopting technologies that will get cheaper in the future. We already face massive economic challenges from an ageing society. We should do our bit, but stop leading with our chin.

In terms of the how, a shift towards a new generation of boring nuclear, built at scale, seems likely to be cheaper and far less risky than an experimental grid with all renewables and to-be invented storage technology.

Given that Ed Miliband’s net zero grid by 2030 will fail, we should instead plan on the basis that we will keep gas around for longer until other technologies mature or appear.

We should work with others like the EU on whether we can implement carbon border taxes - not least to remind other countries to stop free-riding on us. But we should not bank on this idea being any kind of game changer or even working.

The war in Ukraine gave Europe an incredible demonstration of the importance of energy to our lives, and how the price of energy affects the price of everything.

From 2000 to 2019 RPI inflation averaged 2.8%. In 2022 it hit 14.2%.

In 2022 the government had to spend just under £60 billion just to cushion people from the cost of suddenly much more expensive energy. It didn’t make anyone happy or well off, it just averted disaster.

Despite the continuing war, some of those effects have unwound.

But our own policies are slowly and permanently pushing up prices in the way the invasion of Ukraine did quickly.

The only difference is that, like a boiled frog, we don’t notice it as much.

Further reading

Our World In Data - CO2 emissions

James McSweeney: Gone with the Wind

James McSweeney: Ned Zero

David Turver: Lies, damned lies and wind energy lobbyists

Southwood, Hughes and Bowman: Foundations

Nice piece. But the position is hopeless in the face of a massive Green lobby spin campaign, over many years. Comnservative governments have been complicit in this (in fact, actively encouraged it), as has the civil service. The majority of the public and most of the honourable members have now comprehensively drunk the Cool Aid. Finding the truth is difficult. In this instance, people will only start seeking it when the UK's energy situation becomes intolerable.

Given the way the green lobby push for technologies that simply don’t exist, I suspect the actual target they have is de-growth. The answer for this country has been obvious for 20 to 30 years, we need to switch to plentiful electricity from Nuclear power. But that represents an actual solution,hence the green lobby, conservative and labour governments and HMT have been absolutely set against it.